Today's European session began with a correction to the dollar which has strengthened in recent weeks, and according to a new established "tradition", the dollar is declining against the background of falling yields on US government bonds.

As of this writing, the yield on 10-year Treasury bonds was 1.537% (versus a local high of 1.624% last week and versus a multi-year low near 0.500% in August last year). The DXY dollar index hit a 15-week high of 92.52 during today's Asian session, but declined to 92.02 at the start of the European session.

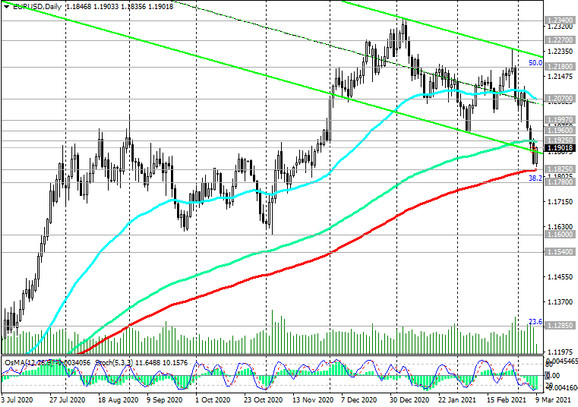

The weakening of the dollar following the fall in the yields of American bonds led to the growth of EUR / USD. The pair rallied to 1.1900 earlier in today's European session, rising from a 4-month low of 1.1836 hit in today's Asian session.

However, many observers tend to assume that this is a temporary strengthening of the euro, which remains vulnerable in cross-pairs with other major currencies, and the growth of the EUR / USD pair. Many market participants believe that on the eve of the ECB meeting, which will take place on Thursday, short positions in the euro and the EUR / USD pair remain preferable.

The recovery of the European economy largely depends on the pace of vaccination, and so far the EU's strategy in this direction has not been successful enough, economists say. In their opinion, if it takes another quarter to lift most of the quarantine measures, and they will be extended until the fall, then it may take a year more to restore the pre-crisis levels.

It is possible that at the ECB meeting on Thursday, the bank's leaders may speak in favor of additional support measures for the European economy, as well as give less optimistic forecasts for its growth, which may cause a weakening of the euro and a renewed decline in EUR / USD.

Meanwhile, the success of US vaccinations and the soon final approval of the $ 1.9 trillion stimulus package in Congress could give the American economy new impetus for further and accelerated recovery from the pandemic. The continued recovery of the US economy and labor market, in particular, is evidenced by data published last Friday, according to which the number of jobs in February grew for the second month in a row, and their growth rates were much faster than those observed earlier in winter.

The unemployment rate in February, according to a report by the US Department of Labor, fell to 6.2%, which is well below the high of 14.8% reached in April 2020, although it remains so far above the levels it was before the pandemic, when unemployment was close to the lowest levels in 50 years.

Easing restrictions on business activity, vaccinating more people and lowering the number of virus infections from January's peak are boosting economic activity and should lead to more sustainable employment and economic growth, economists say.

In turn, the higher rates of recovery of the American economy in comparison with other major economies in the world will stimulate the growth of demand for American assets and the dollar, as the national currency of the United States and the funding currency of the American stock market.

To clarify: the ECB will publish its decision on the key rate and on the deposit rate on Thursday at 12:45 (GMT). According to the ECB leadership, the balance of risks for the economic prospects of the Eurozone "is still shifted to the negative side", and "until inflation is in line" with the target level, which is just below 2%, the rate will remain low.

After Brexit, trade conflicts, factors of political instability in Europe, as well as the growing coronavirus pandemic, due to which European countries are forced to introduce new quarantine restrictions that negatively affect economic activity, are the main threats to the European economy.

During the press conference, which will start at 13:30 (GMT), a new surge in volatility is possible not only in the euro quotes, but also in the entire financial market, if the ECB leaders make an unexpected statement. ECB leaders will assess the current economic situation in the Eurozone and comment on the ECB's rate decision. The soft tone of the statements will have a negative impact on the euro.