The dollar is strengthening, and the DXY dollar index has been growing since the opening of today's trading day, and, since the opening of the European trading session, the dollar's strengthening is gaining momentum.

The dollar index is growing due to the strengthening of the dollar against its main competitors, the euro, yen, pound, whose share in the DXY dollar index is about 58%, 14% and 12%, respectively.

As of this writing, DXY futures are traded near 94.25. Despite the decline from the local multi-month high of 94.52, reached at the end of September, the positive dynamics of the DXY dollar index remains.

According to forecasts, if the situation on the labor market continues to improve, then the Fed may announce the reduction of the bond buyback program at the next meeting, which is scheduled for November 2-3. Reduced liquidity in the market will lead to a new increase in demand for the US dollar, and investors have already begun to build on the possibility of tightening the Fed monetary policy in prices.

Meanwhile, the US dollar is falling against commodity currencies such as the Canadian, Australian and New Zealand dollars, which are largely driven by rising energy prices.

So, the quotes of futures for WTI crude oil, for example, renewed today their highs since November 2014, having risen above $ 80.90 per barrel. Brent crude is also traded today at its highs since October 2018, above $ 83.80 a barrel.

Of the 3 major commodity currencies (Canadian, Australian and New Zealand dollars), the Canadian and Australian dollars show the best dynamics. Canada and Australia are the largest exporters of energy resources: Canada - oil, Australia - coal and liquefied gas.

New Zealand's exports are mainly concentrated on the export of agricultural products from the country (in 2020, 27% of New Zealand's exports were dairy products and other food products of animal origin, 13.5% - meat and edible meat by-products, 7.52% - timber and products from it and charcoal). And the main consumers of New Zealand exports are China (27%), Australia (13.5%), the USA (11%), Japan (with a share of 5.94%).

The restraining factor for a more rapid strengthening of the NZD, oddly enough, was the decision of the Reserve Bank of New Zealand to raise the interest rate (for the first time in 7 years) by 0.25% to 0.5%. The RBNZ meeting ended last week, at which the bank also signaled further tightening of monetary policy next year. The rate was raised to curb inflation and rapidly rising house prices.

The main objectives of the RBNZ are to achieve an annual inflation rate of 2% in the medium term (currently the current inflation expectations are near the upper limit of the target range of 1% -3% set by the RBNZ) and full employment. However, earlier this year, the country's government recommended taking housing prices into account when making monetary policy decisions. Over the past year, the median home price has grown by about 30%, and this growth was one of the strongest in the economically developed countries.

In August, the RBNZ predicted that the key rate would rise to 1.6% by the end of 2022, and to 2.0% in the second half of 2023. The bank will publish new forecasts at the end of November.

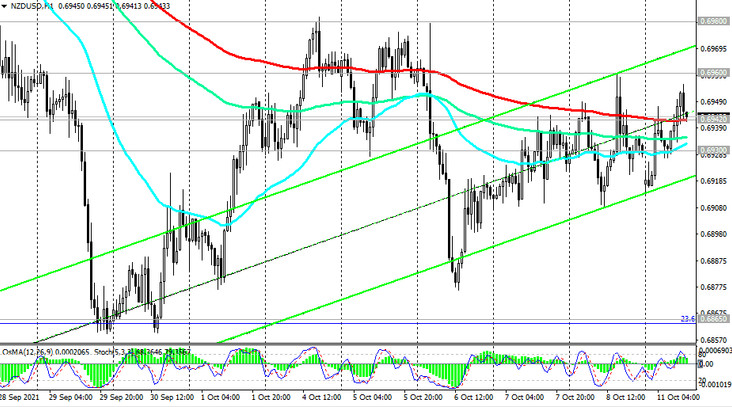

At the time of publication of this article, the NZD / USD pair is near the 0.6942 mark, through which an important short-term support level (EMA200 on the 1-hour chart, EMA50 and the middle of the ascending channel on the 4-hour chart) passes. At the same time, a breakdown of one of the levels 0.6960 or 0.6930 may determine the direction of further short-term dynamics of NZD / USD (see “Technical analysis and trading recommendations”).

Meanwhile, market participants continue to analyze the report of the US Department of Labor published last Friday with data for September. The data was mixed.

Instead of the expected 500,000 growth in the number of new non-agricultural US jobs, the NFP was only +194,000 (the lowest since December 2020), while the unemployment rate fell to 4.8% from 5.2% at the forecast 5.1%.

New data from the US Department of Labor reinforce fears that the coronavirus and global supply problems will continue to stifle the economic recovery.

Now, after the release of key data from the US labor market, market participants will closely monitor the release of important new macro statistics in the US ahead of the November (November 2-3) Fed meeting in order to assess the degree of possibility of reducing the volume of existing stimuli.

Economists believe that the US dollar will continue to strengthen as the Federal Reserve is ready to begin normalizing monetary policy, and US energy independence will protect the country's economy from rising commodity prices.

Therefore, in the dynamics of such pairs as USD / CAD, AUD / USD and NZD / USD, the intrigue will persist, at least in the next few weeks.

And today banks in the United States are closed for the celebration of Columbus Day, which will affect the trading volumes during the American trading session. However, this does not negate the possibility of a sharp increase in volatility in short periods of time. For various reasons: due to speculative actions of market participants or when unexpected news comes out.