According to data released on Tuesday by the US Department of Labor, the final demand index (PPI), which broadly reflects the conditions of supply in the economy, rose +0.8% in November (after rising +0.6% in August, September and October and against forecast +0.5%). On an annualized basis, the figure rose even more, to +9.6% from +8.8% in October. The core PPI, excluding volatile food and energy prices, rose +0.7% in November (after rising +0.4% in October). Previously published information suggests that consumer inflation in the US in November also accelerated (up to 6.8%), core inflation is now also 4.9%.

The presented data on consumer prices and producer prices indicate a continued increase in inflation. Its pressure on prices is obvious and it justifies the expected decision of the Fed to tighten monetary policy, while the American labor market has already returned to a balance sheet with an unemployment rate of 4.2% and the lowest number of new jobless claims since 1969 (published last week data on applications for unemployment benefits showed a decrease in applications to 184 thousand).

Today the attention of market participants will be focused on the Fed meeting and the publication of its decision (at 19:00 GMT) on interest rates. The Fed is expected to double the pace of its stimulus roll-back, cutting $ 30 billion in purchases every month (the bank had previously announced a $ 15 billion monthly cut in purchases), with the program's completion date postponed to March from the summer of 2022. According to economists, the Fed will implement two rate hikes in 2022, then three more in 2023 and four in 2024. However, there is an opinion of economists that this rate of tightening of the FRS monetary policy will not be enough if inflation does not start to slow down. At the same time, the prospect of the Federal Reserve's monetary policy tightening at an increasing pace creates preconditions for the dollar to strengthen.

During today's Asian trading session, the DXY dollar index declined slightly after yesterday's gains to 96.55. At the time of this posting, DXY dollar futures are traded near 96.41, at the top of the range between local highs near 96.94 and local lows near 95.54 reached at the end of November, while remaining in the 16-month local highs and maintaining positive momentum.

Against the background of the dollar weakening during the Asian session, the EUR / USD pair rose. The main rival of the dollar in the currency market, the euro, received support yesterday from the data on industrial production in the Eurozone published by Eurostat. In October, it rose +1.1% after contracting for two consecutive months. During this period, the production of capital goods increased by +3.0%, consumer durable goods - by +1.7%, and other consumer goods - by +0.4%. In annual terms, industrial production grew by +3.3% against the forecast of growth by +3.2%.

At the same time, despite the stabilization in November of the purchasing managers' index (PMI) for the manufacturing sector of the Eurozone (it had been declining for four months), supply chain disruptions continue to worsen. "The strong overall (PMI) reading masks major current concerns for manufacturers", IHS Markit said recently. The increase in the number of Covid-19 infections and the spread of the omicron strain cloud the short-term prospects, creating a threat of further supply disruptions and provoking consumer caution, according to IHS Markit.

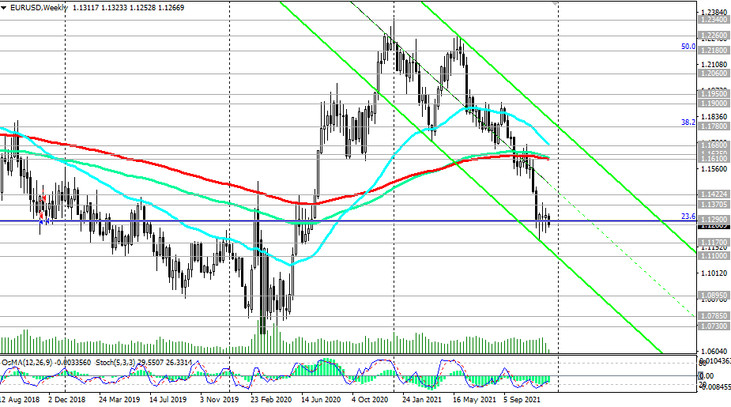

Unlike the Fed, the ECB, which will meet on Thursday, is likely to refrain from any changes in its monetary policy aimed at tightening it in the short term. On Thursday, the ECB is likely to confirm that the PEPP program will end in March, but will be replaced by a third € 300bn buying program to ensure a smooth transition to a smaller asset purchase program, economists said. Such a divergence in the rate of curtailment of stimulus by the Fed and the ECB should put pressure on the pair EUR / USD. The importance of higher Fed interest rates and the prospect of an increasing divergence of interest rates in the United States (in comparison with other economically developed countries of the world) comes to the fore, creating the preconditions for further strengthening of the dollar, including in the EUR / USD pair. Its breakout to the zone below 1.1200 mark will open the way towards further decline, first towards 1.1100, and then, if everything goes according to the scenario described above, towards the March 2020 lows, recorded near 1.0700. Note, just in case, that local multi-year lows were recorded in January 2017, near the 1.0340 mark.

Also recall that after the publication of the decision on interest rates, the Fed's press conference will begin at 19:30 (GMT). Market participants would like to hear from Powell's signals and his opinion on how central bank leaders assess the prospects for raising rates next year. The economic forecasts of the Fed's leaders will also be published today, which may also clarify how they assess the prospects for changing their policy.

The ECB's decision on interest rates and monetary policy statement will be published tomorrow at 12:45 (GMT).