USD Weekly Fundamental Outlook: USD Bull Trend Continues; Fed to Hike 50bp on Wednesday

After correcting lower for 2-3 weeks, the US dollar rebounded strongly and (the DXY index) is now again nearing the yearly highs from May around 105.00. Most of the gains came on Thursday and Friday, incentivized by renewed risk aversion amid selling in global stock markets.

Friday’s hotter than forecasted CPI inflation report provided the additional boost needed for the greenback to resume its uptrend. High inflation will keep the Fed firmly on its hawkish path. A 50bp rate hike is fully expected and priced in by the markets for the meeting this Wednesday. But the Fed will have the chance to send a more hawkish message via the dot plot economic projections and Powell’s press conference. Thus, the dot plot and the forward guidance will again be the key market drivers.

Chances are they will lean heavily on the hawkish side, which is why the dollar is already on the move toward the prior highs. With the strong economy and inflation at the highest in 40 years, the Fed has all the reasons to be aggressively hawkish. This will continue to be a major factor in supporting the USD this year. If the Fed delivers a hawkish message (perhaps by suggesting a 75bp hike is possible), then the USD could reach and surpass the highs from mid-May. This would likely mean that EURUSD slides below the 1.0350 low as well.

There are some economic reports worth watching on the US calendar this week. Retail sales, the Empire State manufacturing index (both on Wed), and the Philadelphia Fed manufacturing index (Thur) are in focus as important indicators for the health of the economy. Various housing data will also be released on Wednesday and Thursday.

EUR Weekly Fundamental Outlook: Euro Plunges Despite Hawkish ECB, EURUSD En Route to Parity

The ECB delivered a hawkish meeting last Thursday, and yet the euro fell sharply by the end of the day. In a recent post, we discussed why the EUR is a lose-lose situation in the current environment, and that scenario now seems to be transpiring.

The culprit behind the EUR’s weakness are the rapidly widening bond yields between Germany and the Southern countries of the Eurozone (Greece, Italy, Portugal). When the ECB hikes rates, it increases the borrowing costs (bond yields) for countries. The problem for Europe is that borrowing costs are increasing much more and much faster for the highly indebted Southern members (Greece, Italy, Portugal) than for the northern states (Germany, the Netherlands). This is problematic because it reduces the ability of weaker (more indebted) Eurozone countries to pay back their debt. This is not a good scenario for the currency as its spurs capital to flee the region and is why the euro fell in spite of the hawkish ECB last week.

The ECB can do something to help Italy and Greece by keeping their borrowing costs artificially low. However, that would include some form of partial QE, which is by itself bearish for a currency. Hence, the EUR’s lose-lose outlook. This dynamic will likely remain a dominant driver for the euro for the time being, and economic data and other developments may matter less. The euro is unlikely to gain much traction over the summer months, and the path to parity for EURUSD seems intact.

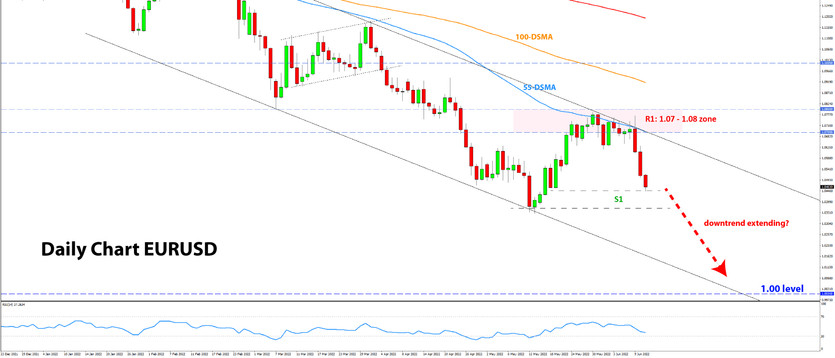

EURUSD Technical Analysis:

EURUSD fell by around 200 pips last week after the retracement topped in the 1.07-1.08 zone around the turn of the month. It has already fallen below the 1.05 level today (Mon), though a break below the 1.05 zone can’t be confirmed at the moment.

Some support may emerge here around 1.05 since it was an important technical zone in the past. However, the sharp declines last Thursday and Friday suggest that it’s less likely this support zone will hold like in the past. And with EURUSD having already broken below the 1.05 level, it could soon reach 1.04 and attack the prior lows of 1.0350.

The support around 1.0350 is unlikely to be strong, as the low is rather insignificant in the larger historical context. Hence, the next important support area below 1.05 is parity (1.00), and it is what traders are likely to focus on. It’s also worth mentioning that the daily chart technicals (bearish channel) show that EURUSD could theoretically reach 1.00 by July 1.

To the upside, resistance remains rock solid at that 1.07-1.08 zone.

GBP Weekly Fundamental Outlook: UK Economy Going from Bad to Worse; BOE Unlikely Save the Pound on Thursday

Boris Johnson survived the no-confidence vote last Monday, but it was with a very narrow margin. As a result, most political analysts now see his days in office to be numbered. Still, UK politics shouldn’t affect GBP much even if Boris Johnson resigns tomorrow, but a weakened Prime Minister certainly cannot be a positive either.

The key event this week is the Bank of England monetary policy meeting on Thursday. They are likely to hike interest rates by 25bp, with the risks tilted for a hawkish message from them as well. Traders will watch the MPC votes to gauge how hawkish/dovish the BOE feels at the moment. However, like the ECB’s case, even a hawkish BOE is unlikely to provide a sustainable boost for GBP because of the deteriorating economic outlook for the UK.

The UK is in stagflation mode (high inflation, low growth), which is rarely a good mix for the currency. Today’s UK economic reports were bad across the board, and the pound sold off sharply (GDP, industrial and manufacturing production all missed estimates poorly). The market will also watch tomorrow’s employment reports, and more negative surprises there could fuel further GBP selling.

Ultimately, the weakening economy is likely to limit any scope for sustained BOE hawkishness, potentially making them shift to a fully dovish stance (rate cuts) as soon as this year. The risk of this scenario is behind most of GBP’s weakness since April. This theme – of course, caused and exacerbated by the Ukraine war and the energy crisis – should keep the pound weak for the foreseeable future.

GBPUSD Technical Analysis:

After the peak of the retracement at the 1.27 zone in late May, GBPUSD first consolidated for 5-10 days before sliding more sharply last week. It is now already trading at the prior lows of 1.2150, with prospects to break below it soon. The bear trend that started back in February is intact, and that falling trendline is holding neatly so far (see chart below).

This 1.2150 area is already attracting some bullish pressures today. However, it is not the most important support zone in the current context. The crucial long-term support for GBPUSD is the major 1.20 area. It is likely to prove a much harder nut to crack than the current 1.2150 zone.

Resistance is now at the 1.25 zone, around the falling trendline of the bear trend. The downtrend here suggests GBPUSD can reach the important 1.20 area by the end of this month.

JPY Weekly Fundamental Outlook: BOJ to Stay Committed to Dovish Policies; Intervention a Growing Risk for JPY Shorts

The yen resumed its steep bear trend following the brief retracement in May as global bond yields (of other advanced nations) surged higher again in response to further rising inflation rates. The uptrends in bond yields are likely to extend, which should keep strong bearish pressures on the yen intact (bullish JPY pairs). USDJPY already breached the 135.00 level this morning.

The sharp extension of the JPY bear trend last week has caused the market to fear intervention from Japanese officials again. In recent days, there were new instances of Japanese officials commenting on the yen’s weakness, which hadn’t happened since May, when the yen was also falling sharply. Though intervention still looks unlikely, such communication suggests that it is becoming more likely by the day and as the yen continues to weaken. This is now quickly becoming the main risk to holding short JPY positions. In case of intervention, the JPY correction can be sudden and violent.

On the other hand, the Bank of Japan remains fully committed to its dovish QE and YCC policies. They will hold their regular meeting on Friday and will likely keep the dovish stance fully intact as they don’t see inflation risks as serious in Japan. This dovishness (considering that other central banks are hawkish) will continue to pressure the JPY.

Given the high volatility in JPY pairs, Fx traders should be cautious and prepared to ride wild swings in both directions. A runaway move higher in JPY pairs (USDJPY quickly to 140.00?) is possible in the current environment as there are no JPY bulls left to hold the market. On the other hand, the risk of Japan’s officials intervening to stop JPY weakness could cause a sharp move in the other direction (USDJPY suddenly back below 130.00?).

USDJPY Technical Analysis:

USDJPY today surpassed and achieved the 20-year high from January/February 2002 at the 135.10 level. This is a huge move, considering that USDJPY was trading around 115.00 in early March.

Naturally, technical indicators like the RSI and Stochastic remain stuck at heavily overbought levels. But overbought conditions don’t mean much when the trend momentum is this powerful. Also plotted on the daily chart below is the ADX indicator. Currently, its reading is at 61, indicating a very strong trend. The slope and separation between the plotted moving average lines (55-day, 100-day, 200-day) also confirm the powerful bullish momentum.

Some retracement or consolidation looks possible here now that USDJPY has tested the significant 135.00 resistance zone. A break below 133.00 – which is where the lows of the previous two days stand – may signal a deeper retracement. In such a scenario, the 130.00 would come into focus as the next support zone (it’s also a 61.8% Fib level).