Despite the fact that the dollar's attractiveness as a defensive asset has declined, it still retains its recently won positions in the foreign exchange market. Against the backdrop of reports from South Africa that the course of the disease of those infected with the new omicron strain has a milder form than with the disease with previously identified strains of coronavirus and against the backdrop of the rhetoric of the adviser to the President of the United States on medical affairs Anthony Fauci, who believes that the new mutation of the coronavirus "omicron” is not more dangerous than other strains, the activity of buyers of risky stock market assets has increased. Over the past 2 trading days, major US and European stock indices have risen significantly. So, since the beginning of this week, the US broad market index S&P 500 has risen by 3.2%, returning to the zone of record highs, and the European EURO STOXX 50 has added 4.3%, completely recouping the losses of the previous month.

The positive sentiment of the stock market participants and their inclination to purchase highly profitable but risky assets persists. The US bond market has also reacted positively to reports of a new strain of coronavirus. Thus, the yield on 10-year US bonds rose yesterday to 1.482% from 1.356% at the end of last week.

At the same time, the DXY dollar index is in no hurry to decline, remaining in the zone of 16-month local highs reached at the end of November near the mark of 96.94: at the time of publication of this article, DXY futures are traded near the mark of 96.21. Although the dollar is becoming less attractive as a safe-haven asset, the prospect of tightening the Fed's monetary policy supports its quotes. The importance of higher Fed interest rates and the prospect of a widening divergence of interest rates in the United States (in comparison with other economically developed countries of the world) are coming to the fore, creating the preconditions for the further strengthening of the dollar.

The continued growth of the US economy, mostly at a faster pace than in Europe, also enhances the attractiveness of US assets, increasing the demand for the US currency. Thus, under the current conditions prevailing in the world economy, it is more logical to expect a further strengthening of the dollar than its weakening.

The next meeting of the Bank of Canada will take place today (we wrote about this in yesterday's review): its decision on interest rates will be published at 15:00 (GMT). And next week, in addition to the FRS, 3 more of the world's largest central banks (Great Britain, the Eurozone and Switzerland) will also hold their regular meetings on monetary policy issues. Market participants expect the FRS to make decisions aimed at accelerating the phasing out of the stimulating policy. As you know, following the meeting that ended on November 3, the Fed leaders decided to reduce the volume of purchases of assets, which amounted to $ 120 billion a month, by $ 15 billion in November and December. In their view, such a cut, "is likely to be appropriate every month", although they are willing to adjust the pace of the curtailment of purchases, "if it is justified in view of changes in the outlook for the economy". If after the December meeting, which will be held on December 14-15, Fed leaders accelerate the pace of reduction in asset purchases, for example, to $ 30 billion a month, then the QE program may be completed by March, which will increase the likelihood of an increase in interest rates in the first half of next year. In particular, at the end of November, the head of the Fed, Jerome Powell, said that inflation should probably not be considered temporary now, since its growth rates have been exceeding the FRS's target level for a long time. "The risk of higher inflation has increased", Powell said at a hearing before the Senate Banking Committee. In this regard, Powell considers it necessary to accelerate the phasing out of economy stimulating. "The economy is in very good shape, inflationary pressures are high, therefore, in my opinion, it is advisable to consider postponing the curtailment of asset purchases, which we actually announced at the November meeting, for a few months earlier", Powell said. And this prospect creates the preconditions for further strengthening of the dollar.

The other aforementioned central banks (ECB, Bank of England and NBS) probably should not be expected the same decisive steps as from the Fed aimed at tightening monetary policy, which will create an advantage in favor of the dollar.

Nevertheless, one should not expect strong growth from the USD / CHF pair so far: the franc is in active demand as a defensive asset.

At the end of November, the State Secretariat of Economic Affairs of Switzerland published a report on the country's GDP. In the 3rd quarter of 2021, Switzerland's GDP grew by +1.7% (+4.1% in annual terms). The data point to the continued recovery of the Swiss economy (in the previous 2nd quarter of 2021, GDP grew by +1.8% and +7.7% in annual terms), which is a positive factor for the franc.

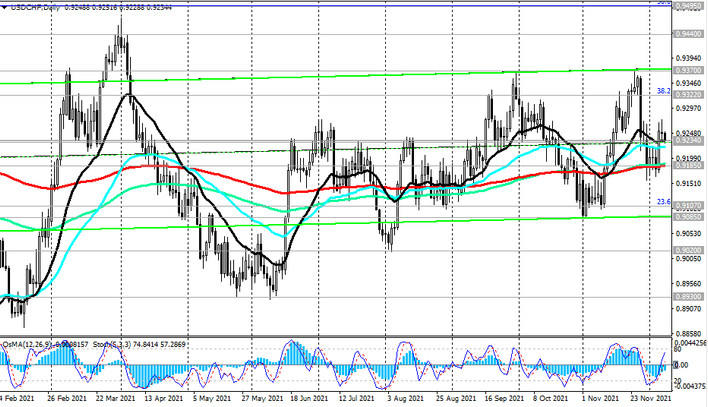

However, USD / CHF should still be guided by its positive dynamics and continued growth, albeit at a more moderate pace. At the moment, this currency pair is traded in the mid-term bull market zone, staying above the key support level 0.9185. If its positive dynamics continue, we should expect growth into the zone of the key long-term resistance level 0.9440, a breakout of which will mean a return of USD / CHF into the zone of the long-term bull market (for more details, see “Technical Analysis and Trading Recommendations”).